Four years of going low carb: four takeaways to digest

As more investors align their portfolios with the goals of the Paris Agreement, many of the world’s most carbon-intensive companies are setting GHG emissions objectives. But what does it mean for a company to transition to the low carbon economy?

As more investors align their portfolios with the goals of the Paris Agreement, many of the world’s most carbon-intensive companies are setting GHG emissions objectives—and a growing number are even committing to net zero targets. But what does it mean for a company to transition to the low carbon economy? And what does a credible commitment look like?

Four years ago, FTSE Russell partnered with the Transition Pathway Initiative (TPI) and the Grantham Research Institute at the London School of Economics to develop a corporate climate action tool that directly addresses these questions. Asset owner-led, the TPI has since become the go-to tool for evaluating what the transition to a low carbon economy looks like for companies with a high impact on climate change—and how prepared they are for the transition.

As the TPI tool has emerged as a leading corporate climate action investor initiative, its growing adoption has revealed four key takeaways. And while some are encouraging, others shed light on the work left to be done:

1. Demand for the right metrics exponential

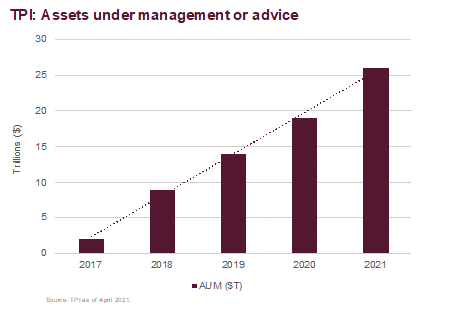

In the four years since its launch, a rapidly growing number of investors have committed to using the TPI tool and its data in a range of ways. They’ve reported the tool has been instrumental in informing their investment research, engaging with companies, and tracking managers’ holdings. Together with FTSE Russell, we also saw the development of the FTSE TPI Climate Index Series, enabling investors to passively track an index that uses TPI inputs to account for the opportunities and risks associated with the low carbon transition.

To date, a total of 106 investors globally have pledged support for the TPI, representing over $29 trillion in combined assets under management. As shown below, this number has risen exponentially since 2017.

2. Net zero is the new 2°C…Not all net zero commitments are created equal

When companies first began setting emissions targets, the majority were targeting the 2°C alignment initially set forth by the Paris Agreement. But TPI data indicates companies are now beginning to commit to net zero emissions by 2050. In fact, among the carbon-intensive companies TPI assessed, the number pledging genuine net zero targets—or targets covering their most material emissions—more than doubled from 2020 to 2021.[1]

But while momentum behind this trend is encouraging, it’s important to note that only 35 of the 292 companies that TPI assessed on carbon performance made genuine net zero commitments. Many more companies have set net zero targets, but they often cover a limited scope of lifecycle emissions. For example, some net zero pledges in the oil and gas sector cover operational emissions, but don’t include downstream emissions from the use of companies’ products. In such cases, a net zero target doesn’t necessarily mean the company’s material emissions will reach net zero and therefore can’t be considered by investors as a credible target.

3. …but alignment still isn’t where is should be

While many of the world’s largest and most carbon exposed companies are committing to emissions targets, TPI’s carbon performance assessment indicates that most companies’ targets aren’t ambitious enough. Among companies who have set emissions targets, only 30% are aligned with the Below 2°C benchmark, just 4% align with 2°C, and 38% don’t align with any benchmark.

Even in cases where emissions targets are aligned, in most sectors companies aren’t reducing emissions fast enough to hit their 2030 targets—and none are on track to meet their 2050 targets. These findings suggest that even those companies that have already set adequate emissions objectives need to accelerate their emissions reduction efforts to meet them.

4. Real change hinges on policy revolution

The upcoming 2021 UN Climate Change Conference (COP26) is expected to have a significant focus on finance but this should not hide the need for ambitious government policy changes as well. Policy and finance have to move in tandem. The steps finance can take are not isolated from the impact of regulation on companies and these have to work together if we are to effectively drive the transition. Companies need an enabling policy environment to help them transition. This is why the TPI assessment includes two indicators that focus on the corporate-policy interface. Companies are asked to disclose their involvement in industry associations that are active in climate lobbying, and to demonstrate support for domestic and international efforts to mitigate climate change. This is an important recognition that companies have influence on the policy environment within which they operate and investors expect alignment of industry lobbying to company commitments to support the Paris Agreement.

Demystifying the low carbon transition for both companies and investors

Over the past four years, companies and investors alike have found huge value in the TPI tool’s ability to demystify what it means for a company to transition in line with the Paris Agreement. TPI has provided companies with clarity as to what investors need to see in their corporate public disclosure and enables them to demonstrate how they’re navigating the transition, whilst at the same time providing investors with a practical tool to drive real world emissions reduction and support portfolio alignment to net zero objectives. The partnership with FTSE Russell has also enabled practical investment applications to come to the market such as the FTSE TPI Climate Transition Index, that provides a way to invest passively to manage the risks and opportunities of the transition whilst also supporting that same transition and corporate engagement initiatives.

[1] Source: Transition Pathway Initiative, TPI State of Transition Report 2021

To learn more about FTSE Russell click here.

© 2021 London Stock Exchange Group plc (the “LSE Group”). All information is provided for information purposes only. Such information and data is provided “as is” without warranty of any kind. No member of the LSE Group make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance. No member of the LSE Group provide investment advice and nothing contained in this document or accessible through FTSE Russell products should be taken as constituting financial or investment advice or a financial promotion. Use and distribution of the LSE Group data requires a licence from an LSE Group company and/or their respective licensors.

_400_250_s_c1.png)